Everything you need to know about the IRS’s new EV tax credit guidance

The US Treasury Department today announced its expected EV tax credit guidance on the battery component and critical mineral sourcing requirements of the Inflation Reduction Act, changing the availability of EV tax credits in the US, with the net effect of reducing tax credit amounts for many vehicles purchased on April 18 or later.

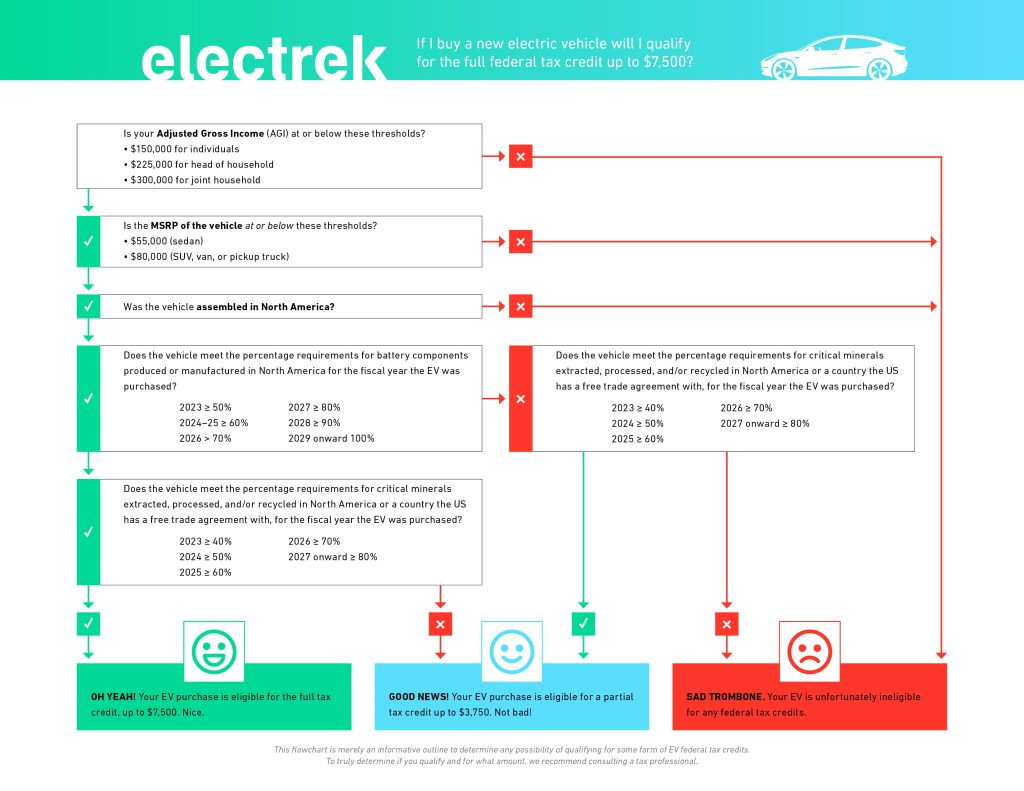

The Inflation Reduction Act includes a provision that limits the $7,500 EV tax credit to vehicles that are assembled in North America. Beyond that, a certain percentage of each car’s battery components need to be built in North America, and critical minerals need to be sourced from the US or a US free trade country, with these percentages increasing every year. Each of these two requirements make up half of the credit, so if a car qualifies for one but not the other, it’s eligible for $3,750 worth of federal tax credits.

The NA-assembled provision went into effect immediately in August when the bill was signed, but the battery sourcing provisions were left up to the Treasury to decide. It was originally supposed to announce those specifics by December, but pushed back the deadline until today.

This temporarily qualified some vehicles, like the Chevy Bolt (which will now remain a screaming deal through April 17), and some Tesla models for the full $7,500 credit. Both GM and Tesla have previously stated that they don’t expect to qualify for the full purchase credit when the new battery rules go into effect.

Senior administration officials advised that while fewer cars will qualify for the full credit in the short term, the law will work to strengthen the US industrial base and eventually there will be more cars that qualify as production gets on-shored.

In addition to the NA-assembly and battery provisions, cars over $55K and SUVs/trucks over $80K MSRP do not qualify. Also, taxpayers cannot claim the credit if their income is over $150K/$225K/$300K for single/head-of-household/married filing jointly.

The domestic assembly provisions caused some rankling in the international community when the bill was passed, with some foreign automakers and governments decrying it as a protectionist move. Since then, to help smooth over these complaints, the US signed a free trade deal for battery minerals with Japan earlier this week and is working on a similar agreement with Europe.

The Treasury has also suggested that it is still possible for foreign-assembled cars to still qualify for commercial tax credits if they’re leased, an interpretation that was pushed for by Hyundai and Kia (but opposed by the famously anti-EV Toyota). In this case, a dealership would file for the commercial credit and presumably could pass it on to the consumer in the form of lower lease payments.

Senior Treasury and White House officials said today that due to the domestic production provisions of the IRA, $45 billion worth of new electric car manufacturing investments have been announced since the act was signed. The administration said this accounts for tens of thousands of jobs across 24 states, along with several other commitments related to the law’s EV-adoption goals (more public charging, more electric transit, and so on).

Details of the new battery sourcing requirements

Thankfully, the new battery sourcing guidance today held few surprises. It is, however, going into effect a little later than expected: April 17, rather than the end of March (today).

So buyers will have a couple more weeks to purchase an EV before tax credit amounts are reduced, as the new guidance will be applicable to vehicles placed into service on April 18 or later. These vehicles may lose access to half or all of the tax credit, depending on where their battery components and critical minerals are sourced.

To meet requirements set up in the IRA, manufacturers must ensure that battery critical minerals are “extracted or processed in the US or any country with which the US has a free trade agreement,” or recycled in North America. They must also ensure that battery components are “manufactured or assembled in North America.”

Each of these legs accounts for half of the total $7,500 credit.

Each leg also has an “applicable percentage” based on the year the vehicle is “placed into service,” which can be seen in the flowchart below. The process of measuring whether a car meets these requirements is relatively straightforward, and involves identifying the value (rather than weight or volume) of each component or mineral used in the battery supply chain:

The Treasury seems like it intends to take a lenient view of what counts as a “free trade agreement” for the critical mineral provisions, and specifically noted that this week’s agreement with Japan counts. The list of countries it identified was: Australia, Bahrain, Canada, Chile, Colombia, Costa Rica, Dominican Republic, El Salvador, Guatemala, Honduras, Israel, Jordan, Korea, Mexico, Morocco, Nicaragua, Oman, Panama, Peru, Singapore, and Japan

There is one more consideration: After 2024, batteries must contain no components whatsoever that were manufactured or assembled by a “foreign entity of concern” (FEOC) and after 2025, no critical minerals can be extracted, processed, or recycled by a FEOC.

The law itself does not specify a full list of FEOCs, so it falls upon the Treasury to provide that before the end of the year, when the rule first takes effect. The Treasury could not tell us whether this list would focus on national or subnational entities.

Presumably, some significant percentage of those entities will be associated with China, given that the IRA specifically intends to reduce the overreliance on China for batteries, whether the list ends up including all of China itself or not. A senior administration official specifically noted that many minerals currently get extracted in Australia and processed in China. The administration hopes some of those minerals could instead be processed perhaps in Japan, under the US’s newly signed trade agreement focused on environmental standards and workers’ rights.

And there is still a chance to iron out any wrinkles left in today’s guidance, as today’s rule is merely a “proposed” rule, rather than a final one. The proposed rule is published in the federal register, and public comments will be taken through June 16. This also means that vehicles placed into service between April 18 and whenever the final rule goes into effect will use the proposed rule, whereas later vehicles will use the final rule, in whatever form that rule takes. Any changes are likely to be minor.

With the new tax credit guidance only released today, a full list of qualifying vehicles is not yet available. Manufacturers will have to certify that their cars meet these new sourcing requirements and submit that information before the proposed rule goes into effect on April 17. The government will publish a list of eligible vehicles and the amount of credit each vehicle receives on fueleconomy.gov on April 18, and we at City Dwellers will keep you updated when that list comes out.

City Dwellers’s Take

With today’s battery sourcing guidance, we’ve moved one step closer to the end of the long and complicated EV tax credit implementation saga. Most provisions of the Inflation Reduction Act are now somewhat clear, with the primary exception of the future point-of-sale tax credits, slated for 2024, which will allow buyers instant access to EV discounts instead of having to wait to file their taxes.

There will be a few more changes over time, as manufacturers move to onshore production, or as the US government possibly makes more deals with other countries as it did with Japan this week. These should gradually qualify more cars for tax credit access.

On the other hand, some cars might lose out over time due to increases in the “applicable percentage” as years tick by. We’ll keep you updated about any changes as we learn about them, but hopefully things will settle into a bit more of a steady state from here on out.

It would have been nicer if the journey was a little simpler, but given that the legislation had the goal of not only increasing electric car adoption but also increasing American manufacturing in a world where manufacturing is so globalized, it was always going to end up being a little complex.

And in the end, more cars will take advantage of the tax credit than before, when credits were capped at 200,000 per manufacturer, so it’s still an improvement, if an imperfect one.

FTC: We use income earning auto affiliate links. More.